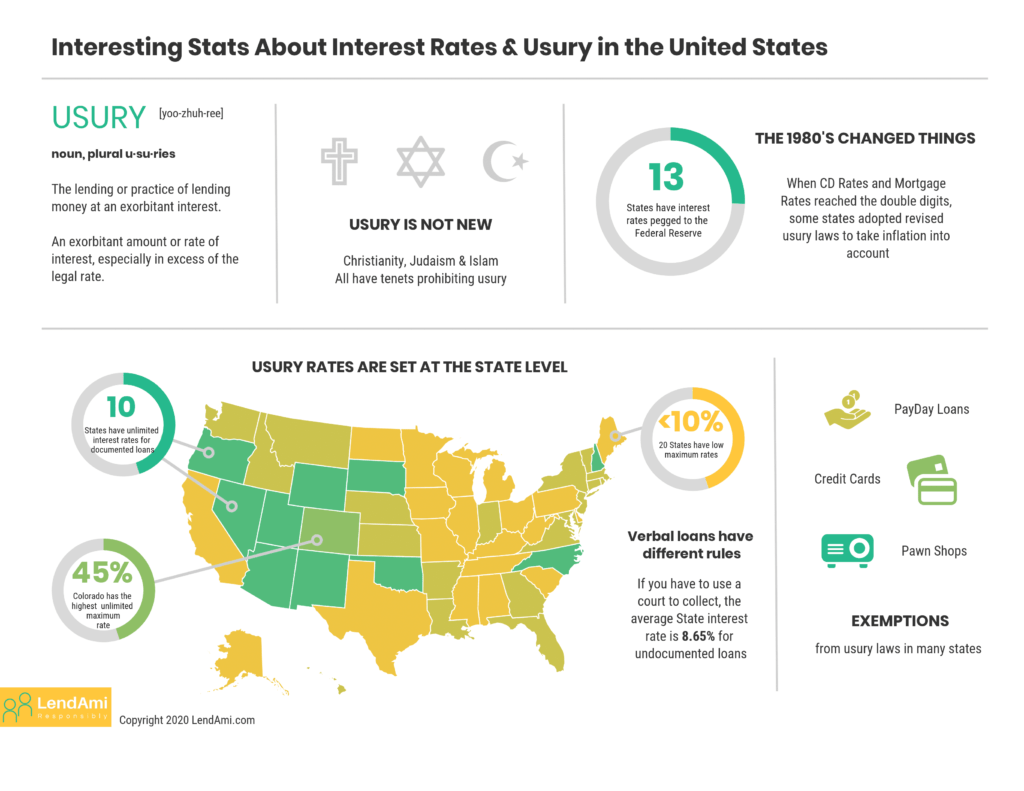

Our usury infographic provides a glimpse into the history of usury as well as the landscape of what the various states charge as their maximum interest rates.

In lieu of a national interest rate, each state has its own laws on maximum interest rates and usury. The maximum interest rate for a personal loan is dictated by the state in which the lender is. This leads some lenders, such as revolving credit card companies, to incorporate and do business in states with the most favorable laws.

The maximum interest rates permitted can vary widely and are generally used for personal loans. Oftentimes, different rates and laws are created for mortgages, payday loans, pawn brokers and business loans.

Laws range from the most basic to very complex. For example, six states have stated maximum interest rates allowed but, if the loan is over a certain amount, the maximum rate can be whatever the parties agree to in writing.

In cases where no written agreement or contract is in place (the loan was made verbally) then the maximum interest rate is typically on the low end of the scale. Think 5% in many cases and upwards of 10 or 12% in some states. This rate comes into play in the event there is a court battle over the loan. When a judgment is handed down, the maximum non-documented interest rate is the default guidance.

Interested in learning more? Check out our interest rate and usury statistics infographic for some other fun facts:

Additional Resources